Customer success story: hyperscale services provider

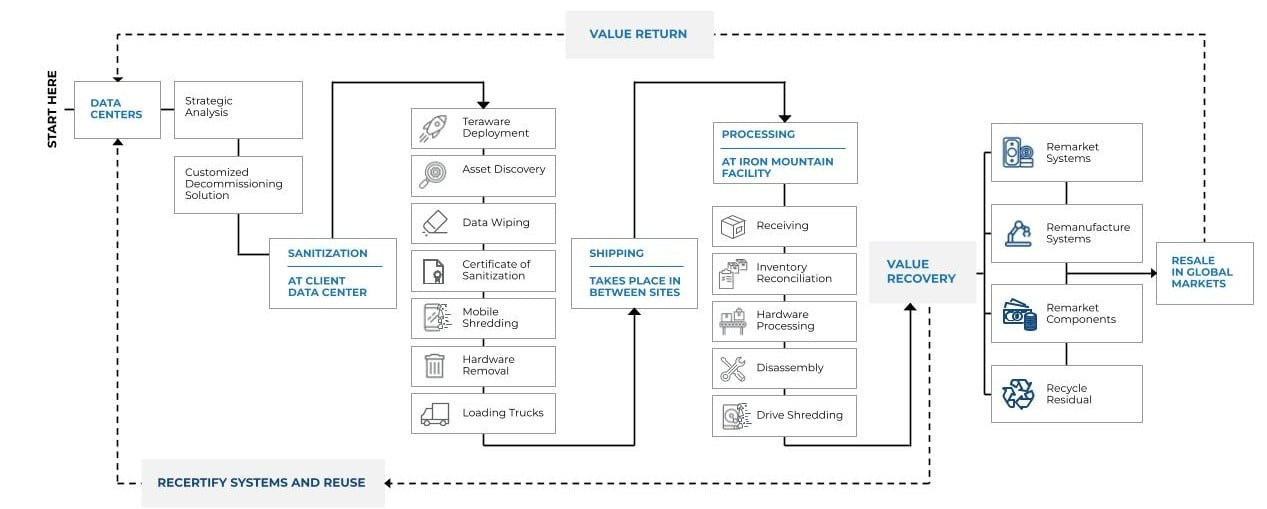

Challenge

Arrival of new servers and storage, which were rapidly losing value while waiting for installation, placed a premium on accelerating decommissioning for this hyperscale services provider. While the nature of the business mandated maximum data security, the provider needed return on investment from asset remarketing to help fund increased tech refreshes.

Solution

Iron Mountain’s custom data center decommissioning services safely, securely, and efficiently executed comprehensive data erasure, uninstallation, removal, and secure shipment of equipment to state-of-the-art processing facilities for remarketing.

Results

All racks were data-free and ready to be wheeled out four days after the project started. All assets were removed from the client site within 14 days. Remarketing the retired assets netted the client several million dollars, helping to close budget gaps.